Property Launches & Investments

This is some blog description about this site

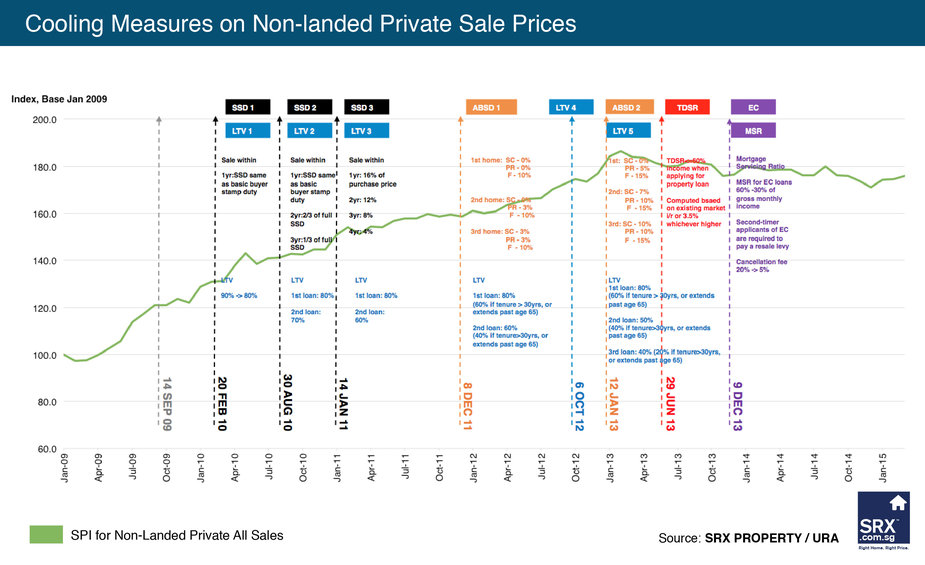

Singapore Property Market Cooling Measures

- Font size: Larger Smaller

- Hits: 3658

- 0 Comments

- Subscribe to this entry

- Bookmark

Below is a comprehensive view of the latest government policies related to the residential property market. These policies are often referred to as the 'Property Market Cooling Measures'.

Select index benchmark:

» Click to Calculate your Stamp Duty.

A Brief Summary of Cooling Measures

1. Additional Buyer's Stamp Duty (ABSD)

| Citizenship | ABSD Rate on Primary Home Purchase | ABSD Rate on Secondary Home Purchase | ABSD Rate on Tertiary & Subsequent Purchase |

|---|---|---|---|

| Singapore Citizens | N/A | 0% revised to 7% | 3% revised to 10% |

| Permanent Residents | 0% revised to 5% | 3% revised to 10% | 3% revised to 10% |

| Foreigners1 and non-individuals | 10% revised to 15% | 10% revised to 15% | 10% revised to 15% |

Note:1.Citizens of the USA, Switzerland, Liechtenstein, Norway, Iceland will be treated the same as Singapore Citizens due to FTA agreement.

2. Sellers' Stamp Duty (SSD)

| Residential Property Sold In | Year 1 | Year 2 | Year 3 | Year 4 |

|---|---|---|---|---|

| SSD Rate since Feb 2010 | Same as basic Buyer Stamp Duty |

N/A | N/A | N/A |

| SSD Rate since Aug 2010 | Same as basic Buyer Stamp Duty |

2/3 of basic Buyer Stamp Duty |

1/3 of basic Buyer Stamp Duty |

N/A |

| SSD Rate since Jan 2011 | 16% | 12% | 8% | 4% |

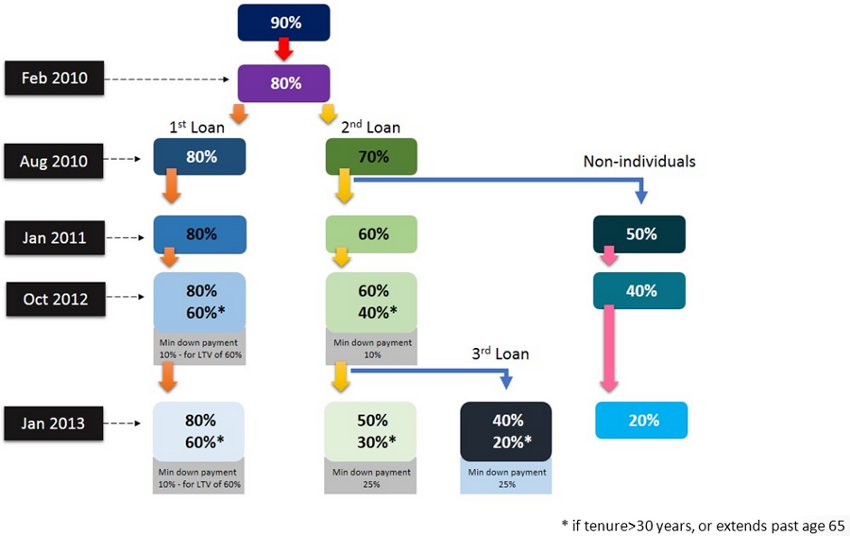

3. Loan-to-Value (LTV) Ratio

Source: SRX / StreetSine

Policy Details

| Effective Date | Major Cooling Measures that Affect Residential Property Market |

|---|---|

| 9 December, 2013 | 1. Reduction of Cancellation Fees From 20% to 5% for Executive Condominiums. |

| 2. Resale Levy for Second-Timer Applicants - Formerly second timers are not required to pay a levy. This is applicable to only new EC land sales which are launched on or after 9th December 2013. |

|

| 3. Revision of Mortgage Loan Terms - From a previous mortgage servicing ratio (MSR) level of 60% to now 30% of a borrower's gross monthly income. The MSR cap will apply to EC purchases from 10th December 2013 onwards. |

|

| 27 August, 2013 | 1. Singapore Permanent Resident Households need to wait three years from the date of obtaining SPR status, before they can buy a resale HDB flat. |

| 2. Maximum tenure for HDB housing loans is reduced from 30 years to 25 years. The Mortgage Servicing Ratio (MSR) limit is reduced from 35% to 30% of the borrower's gross monthly income. | |

| 3. Maximum tenure of new housing loans and re-financing facilities granted by financial institutions for the purchase of HDB flats (including DBSS flats) is reduced from 35 years to 30 years. News loans with tenure exceeding 25 years and up to 30 years will be subject to tighter LTV limits. | |

| 29 June, 2013 | 1. TDSR: Financial institutions are required to consider borrowers' other outgoing debt obligations when granting property loans. His total monthly repayments of his debt obligations should not exceed 60 per cent of his gross monthly income. |

| 2. In particular, MAS requires: -borrowers named on a property loan to be the mortgagors of the residential property for which the loan is taken; -"guarantors" who are standing guarantee for borrowers otherwise assessed by the financial institutions at the point of application for the housing loan not to meet the TDSR threshold for a property loan to be brought in as co-borrowers; and -in the case of joint borrowers, that financial institutions use the income-weighted average age of borrowers when applying the rules on loan tenure. |

|

| 12 January, 2013 | 1. ABSD: Citizens pay 7/10% on second/third purchase (from 0/3%); Permanent Residents (PR) pay 5/10% for first/second purchase (from 0/3%); foreigners and non-individuals now pay 15%. |

| 2. LTV for second/third loan now 50/40% from 60%; non-individuals' LTV now 20% (from 40%). | |

| 3. Mortgage Servicing Ratio (MSR) for HDB loans now capped at 35% of gross monthly income (from 40%); MSR for loans from financial institutions capped at 30%. | |

| 4. PRs no longer allowed to rent out entire HDB flat. | |

| 6 October, 2012 | 1. Mortgage tenures capped at a maximum of 35 years. |

| 2. For loans longer than 30 years or for loans that extend beyond retirement age of 65 years: LTV lowered to 60% for first mortgage and to 40% for second and subsequent mortgages. | |

| 3. LTV for non-individuals lowered to 40%. | |

| 8 December, 2011 | 1. ABSD introduced for further cooling measures: - Foreigners and non-individuals pay 10%, PRs buying second and subsequent property pay 3%, Singaporeans buying third and subsequent property pay 3%. |

| 2. Developers purchasing more than four residential units and following through on intention to develop residential properties for sale would be waived ABSD - To qualify, developers have to produce proof of development and sale within five years. |

|

| 14 January, 2011 | 1. Holding period for imposition of SSD increased to four years from three. |

| 2. SSD rates raised to 16%, 12%, 8% and 4% of consideration. | |

| 3. LTV lowered to 60% from 70% for second property. | |

| 4. LTV for non-individual residential purchasers capped at 50%. | |

| 30 August, 2010 | 1. Holding period for imposition of SSD increased to three years from one. |

| 2. Minimum cash payments raised to 10% from 5% for buyers with one or more outstanding housing loans. | |

| 3. LTV lowered to 70% from 80% for second properties. | |

| 20 February, 2010 | 1. Introduction of SSD for residential property and land sold within one year of purchase. |

| 2. LTV lowered to 80% from 90% on all housing loans except HDB loans. | |

| 14 September, 2009 | 1. Interest absorption scheme (deferment of instalments until TOP) and interest-only housing loans (interest payment only until TOP) were scrapped for all private properties. |

Tagged in:

Additional Buyers Stamp Duty ABSD

Effective dates of measures policy

Loan to Value ratio LTV

Sellers Stamp Duty SSD

Singapore property marketing cooling measures

District 1

Marina Bay Condo | Shenton Way Commercial | Marina Bayfront Condo | Central Boulevard Condo | Central Boulevard Towers | Marina View | V on Shenton | Marina South Pier Condo | Marina One Residences | Shenton Way Condo |

District 2

Pearl Bank En Bloc | Outram Park MRT Condo | Silat Residences | Avenue South Residence | Sky Everton | Sky Everton Freehold Condo Prices | Outram Road Condo | One Pearl Bank | Excellent Connectivity from One Pearl Bank | One Pearl Bank Design and Layouts | Pearl Bank Apartments | Asia Gardens | Anson Road Condo | Tanjong Pagar Condo | Tanjong Pagar Commercial | Greater Southern Waterfront | Wallich Residence | Tanjong Pagar Centre |

District 3

Queenstown Condo | Queens Peak Condo | Dundee Road Condo | Margaret Ville | Margaret Drive Condo | Alexandra View Condo | Prince Charles Crescent Condo | Rest of Central Region Condo | Principal Garden | Silat Avenue Condo | Jalan Bukit Merah Condo | Kampong Bahru Road Condo | Stirling Road Condo | Stirling Residences | Commonwealth Avenue Condo | The Crest @ Prince Charles Crescent | Commonwealth Towers | Highline Residences | Alex Residences |

District 4

Corals at Keppel Bay | Skyline Residences | Reflections at Keppel Bay |

District 5

Park West Condominium En-Bloc | West Coast Vale Condo | Park West Condominium | Parc Clematis | Parc Riviera | The Trilinq | Bijou | West Coast Way Condo | One Normanton Park | Normanton Park Condo | Clementi Avenue 1 Condo | Jalan Lempeng Condo |

District 7

CityGate Condo | Selegie Road Condo | Sophia Road Condo | Tan Quee Lan Street Condo | The M | Middle Road Condo | South Beach Residences | Duo Residences | Beach Road Bugis Rochor Condo | Midtown Suite | Midtown Bay | Midtown Bay Floor Plans and Facilities | Beach Road Commercial | Golden Mile Complex | Textile Centre | Golden Mile Complex En Bloc | Textile Centre En Bloc | The Oasis |

District 8

Peace Centre Mansions En Bloc | Perumal Road Condo | Northumberland Road Condo | Uptown at Farrer | 1953 Condo | LYF | Tessensohn Residence |

District 9

Cairnhill Mansions En Bloc | Orchard Bel-Air En-Bloc | Pacific Mansions En Bloc | Robertson Quay Condo | Paterson Road Condo | Cavenagh Gardens En-Bloc | Cavenagh Gardens | Cavenagh Road Condo | Orchard Boulevard Road Condo | Orchard Road Condo | Scotts Road Condo | Cairnhill Road Condo | Riviera Point | The Iveria | The Iveria Condo Floor Plans | Cairnhill Mansions | One Tree Hill | River Valley Road Condo | Martin Place Condo | Martin Modern | Kim Seng Road Condo | Handy Road Condo | Haus on Handy | Jiak Kim Street Condo | Riviere Condo | Fraser Residence Promenade | Avenir Condo | Pacific Mansions | Great World MRT Station Condo | Martin Place Residences | The Rise at Oxley Residences | Orchard Paterson Cairnhill Road Condo | Core Central Region Condo | Robertson Quay Condo | Paterson Collection | St Thomas Walk | Leonie Hill Road Condo | Horizon Towers | Leonie Gardens | New Futura | Cairnhill Nine | 3 Orchard by the Park | Twin Peaks |

District 10

Grange Road Condo | Farrer Road Condo | Tulip Gardens En Bloc | Tulip Garden Residences | Leedon Green | Leedon Green Floor Plans | Tulip Garden Residences Floor Plans | Tulip Garden | Tanglin Road Condo | Jervois Gardens | Crystal Towers | Juniper Hill Condo by AllGreen Properties | Juniper Hill | The Hyde at Balmoral | The Hyde | Balmoral Road Condo | Jervois Road Condo | Petit Jervois | Jervois Prive Exclusive Condo | Jervois Prive | Jervois Treasures Condo Floor Plans | Jervois Treasures | Tanglin Shopping Centre En Bloc | Tanglin Shopping Centre | Jervois Gardens En Bloc | Spring Grove En Bloc | Spring Grove | Hallmark Residences | Wilshire Residences | Sloane Residences | Ewe Boon Road Condo | Bukit Timah Road Condo | Bukit Timah Collection | Cluny Park Residence | Cuscaden Road Condo | Petit Cuscaden | Cuscaden Reserve | Cuscaden Reserve Condo Floor Plans | Boulevard 88 | Pollen and Bleu | Leedon Residence | Gramercy Park | Ardmore Three 3 | Sculptura Ardmore | RV Residences | Robin Residences | 18 Nouvel@ Anderson Road | Holland Road Condo | The Estoril | The Estoril En Bloc | Hollandia En Bloc | Hyll at Holland | Hollandia | TwentyOne Angullia Park | D'Leedon | Mon Jervois | Holland Village Residences | One Holland Village | One Holland Village A Mixed Development Design | Holland Village Condo | Van Holland | Van Holland Floor Plans | 15 Holland Hill | 15 Holland Hill Floor Plans |

District 11

Chancery Court En Bloc | Chancery Court Condo | Thomson Road Condo | Novena Condo | Newton Road Condo | Pullman Residences | Pullman Residences Floor Plans | Dunearn Road Condo | 386 Dunearn | Dunearn Court Condo | Derby Court | Fyve Derbyshire | Derbyshire Road Condo | Kampong Java Road |

District 12

Balestier Road Condo | Toa Payoh Condo | Neem Tree | Riverbay | Boon Teck Towers | Eight Riversuites | Boon Teck Towers En Bloc | Gem Residences | Kallang Riverside Condo |

District 13

Woodleigh Residences | Upper Serangoon Road Condo | Park Colonial | Woodleigh Lane Condo | Mattar Residences | Woodleigh MRT Condo | Woodleigh Condo | Woodleigh Link Condo | Bidadari New Estate Condo | Upper Aljunied Road Condo | Tre Ver | Raintree Gardens | Potong Pasir Avenue 1 Condo | Potong Pasir Condo | The Maisons | The Quinn | Mattar Road Condo | The Poiz Residences | The Venue Residences | Sant Ritz |

District 14

Eunos Condo | Eunos MRT Condo | Sims Avenue Condo | Changi Road Condo | Parc Esta | Eunosville | Eunosville En Bloc | City Plaza | City Plaza En Bloc | Paya Lebar Road Condo | Sims Drive Condo | Park Place Residences | Paya Lebar Quarters | Sims Avenue Condo | Paya Lebar Central |

District 15

Dunman Road Condo | Coastline Residences | Amber Sea | One Meyer | Albracca | Siglap MRT Station Condo | Marine Parade Road Condo | Casa Meyfort Condo | Meyer Mansion Floor Plans | Meyer Mansion | Meyer Modern | Nanak Mansions | Meyerhouse Exclusive Condominium | Meyerhouse | Meyerbank | Nyon | Rebirth of Amber Park Condo | Amber Park Condo Seafront Living | Amber Park | The Opus | Parkway Mansion | Amber Park En Bloc | Hawaii Tower En Bloc | Parkway Mansion En Bloc | Albracca En Bloc | Laguna Park | Laguna Park En Bloc | Tanjong Katong MRT Station Condo | Meyer Road Condo | Hawaii Tower | Katong Park MRT Condo | Katong Park Residences | Katong Park Towers | Amber Gardens Condo | Amber Road Condo | Neptune Court | Neptune Court En Bloc | Lagoon View | Lagoon View En Bloc | East Coast Marine Parade Condo | Katong Shopping Centre | Katong Shopping Centre En Bloc | Mountbatten Road Condo |

District 16

Siglap Road Condo | Mandarin Gardens | Mandarin Gardens En Bloc | New Upper Changi Road Condo | The Glades | Bedok South Condo |

District 17

The Inflora |

District 18

Tampines Court | Treasure at Tampines | Tampines Court En Bloc | Tampines Street 11 Condo | Tampines Avenue 10 Condo | Coco Palms |

District 19

Florence Regency En-Bloc | Florence Residences Condo Club | Florence Regency | Rio Casa | Kensington Park En-Bloc | Kensington Park | Serangoon Ville | Serangoon Ville En Bloc | Forestwood Residences | Hougang Avenue 2 Condo | Hougang Central Condo | Hougang Condo | Riverfront Residences | Hougang Avenue 7 Condo | Affinity | Serangoon North Avenue 1 Condo | The Garden Residences | New Condo | Serangoon Gardens Condo | Serangoon Central Condo | Lorong Lew Lian Condo | Riverbank Sengkang West Way Condominium | Yio Chu Kang Road Condo | Toho Green | Rivertrees Residences | Parc Botannia | Fernvale Road Condo | High Park Residences | Sengkang West Condo | New Tampines Road Condo | Kingsford Waterbay | Botanique at Bartley | Buangkok Condo | Buangkok MRT Station Condo | Sengkang Central Condo | Sengkang Grand Residences | Sengkang Central Residences | Sengkang Central Residences Floor Plans | Sengkang Grand Residences Floor Plans | Sengkang Central Residences Prices | Sengkang Grand Residences Prices |

District 20

Marymount Road Condo | Braddell View En Bloc | Lentor Hill Road Condo | Lentor Central Condo | Braddell View | Shunfu Road Condo | Jade Scape | Far Horizon Gardens | Far Horizon Gardens En Bloc | Ang Mo Kio Avenue 9 Condo | Faber Gardens | New Lorong Puntong Condo | Thomson Impressions Condo | Adana | Panorama | Upper Thomson Road Condo | Yio Chu Kang Road Condo | Lentor Road Condo | Caldecott Condo | Bishan Central Condo | Lentor Drive Condo |

District 21

Jalan Anak Bukit Condo | Beauty World Condo | Goh & Goh Building En Bloc | Pine Grove | Pine Grove Condo | Pandan Valley Condo | Ridgewood Condo | Ridgewood Condo En Bloc | Mayfair Collection | Mayfair Gardens Condo | Mayfair Modern | King Albert Park MRT Station Condo | Mount Sinai Condo | Ulu Pandan Road Condo | Pine Grove En Bloc |

District 22

Jurong Condo | Lake Grande Condo | Lakeville | J Gateway |

District 23

Toh Tuck Road Condo | Kismis View | Dairy Farm Road Condo | Dairy Farm Residences | Dairy Farm Residences Floor Plans | Foresque Residences | The Lanai | Hillion Residences | Bukit Batok Condo | Hillview Rise Condo | Dairy Farm Residences Prices |

District 25

Woodlands Square Condo | Woodlands Square Commercial | Woodlands Central Condo |

District 26

Springside Road Condo |

District 27

NorthPark Residences | Canberra Drive Condo Sembawang | Canberra Link Condo Sembawang | New Yishun Ave 4 Condo | The Wisteria | Condominium Yishun Central | Symphony Suites | Yishun Avenue 9 Condo | Sembawang Road Condo |

District 28

Jalan Kandis Condo | Kandis Residence |

Executive Condo

Parc Life EC | Choa Chu Kang Drive EC | Sol Acres EC | The Vales EC | Tampines Avenue 10 EC | Tampines Street 62 EC | Fernvale Lane EC | Tampines EC | Signature at Yishun | Choa Chu Kang Grove EC | Bukit Batok EC | Tengah EC | Choa Chu Kang Avenue 5 EC | Woodlands Avenue 12 EC | Sembawang Avenue EC | The Visionaire | New EC at Canberra Link | Canberra Link EC Sembawang | Parc Canberra | Yishun Avenue 9 EC | Yishun Street 51 EC | The Criterion EC Yishun | Yio Chu Kang Road EC | New EC | Serangoon North EC | Yishun Avenue 1 EC | The Terrace EC Punggol | The Amore EC Punggol | Westwood Residences EC | Anchorvale Lane EC Sengkang | Sungei Punggol Reservoir EC Sengkang | Anchorvale Street EC Sengkang | Ola EC | Ola EC Prices and Floor Plans | Westwood Avenue EC | Choa Chu Kang Way EC | Canberra Drive EC Sembawang | BrownStone EC | Choa Chu Kang EC | LakeLife EC Jurong | Jurong EC Jurong | Punggol Drive EC Punggol | Woodlands Avenue 5 EC Woodlands | Parc Canberra Floor Plans | Sumang Walk EC Punggol | Piermont Grand | Piermont Grand EC Prices | Punggol Central EC Punggol |